GSA: “The Semiconductor Industry must reinvent itself in order to survive”

30 March, 2016

A GSA study estimates that the industry will adopt revolutionary new business models: open source chips, new computer architectures, cheap micro-fabs and the long awaited boom in FPGA market

A GSA study estimates that the industry will adopt revolutionary new business models: open source chips, new computer architectures, cheap micro-fabs and the long awaited boom in FPGA market

The semiconductor industry undergoes deep changes and is about to grow again after it will adopt innovative technologies and revolutionary business models. This is the conclusion reached by the Global Semiconductor Alliance research team, trying to foresee the future of the semiconductor industry, following an intense year that has seen the halt of a long growth trend, as well as mergers and acquisitions of unprecedented scale.

Growth has come to a halt

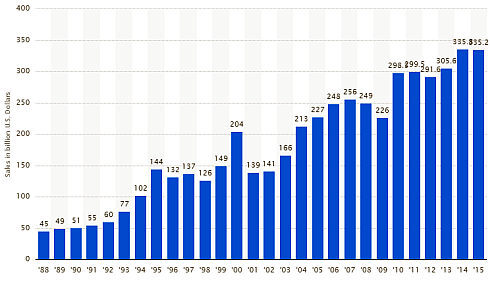

Although cyclical nature, the Semiconductor industry has managed to keep a 50 year growing trend. In the last decade alone it has expanded by approx. 50%, reaching an unprecedented sales record of $340 Billion in 2014. But moving to 2015, sales have decreased by 1.9%, and WSTS estimates a partial recovery of 1.4% to a sales totaling $341 billion in 2016.

A study by the Stanley Morgan investment bank gives a different perspective: only 5% of 2015 public offerings (IPO) were of semiconductor companies, compared to 25% a decade ago.

It seems that investors had the feeling: GSA study shows that only 37% of semiconductor companies went public in the last 5 years, have achieved a higher share price than the initial public offering. The semiconductor industry is lagging behind in further aspects: during 2004-2014, the global economy grew 6% annually, while the semiconductor industry has achieved only 4.4% growth per year.

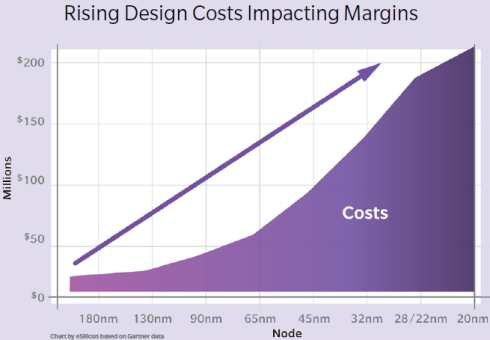

A major contributor to the current crisis is the steep rise in the production and development costs. Two decades ago, a semiconductor development project required an investment of less than $50 million. Today such projects needs as much as $200 million. Additionally, the dazzling proliferation of IP sources undermines the ability to stick to the original schedule.

This is the background for the 2015 wave of mergers in the semiconductor industry. That year has seen acquisitions and mergers amounting to $117.1 billion – five times more than 2014, which has seen transactions totaling $19.9 billion.

China push the market prices

IC Insights maintains that mergers allow companies to keep growing, without making the massive investments needed in order to develop new products and new components in advanced technologies. It believes that the huge values of some of these big deals stems from developments in China.

“The Chinese government has decided to establish an independent semiconductor industry. In order to achieve this, they have instructed government investment funds such as the Tshingua Unigroup to pursue an aggressive acquisition policy abroad. The Chinese course of action pushes the value of most of the main companies considered for purchase.”

The GSA report asks how these developments are going to affect the semiconductor’s industry business model. Some of the answers lie in the past: fierce competition and a drop in profit margins have led to the rise of the Fabless model in which the semiconductor producer outsource the production to an external manufacturer such as UMC, TSMC, GlobalFoundries or the Israeli TowerJazz.

The Fabless model has dramatically reduced market entry costs, and proved to be extremely successful: Fabless companies’ sales comprise today 40% of the semiconductor industry total sales. At the same time, we have seen the rise of intellectual property suppliers taking the concept to the extreme, focusing on the sale of intellectual property to semiconductor vendors. Companies such as ARM, Synopsis, Imagination and Israeli CEVA, have won themselves a central place in the modern chip industry.

Open Source Chips

Which business models will emerge from the current crisis? One might be based on the open source model. This model has done exceedingly well in the software industry. Today, 95% of internet servers run on Linux open system. Approx. 85% of all the smartphones run the open source Android operating system. Red Hat, a company specializing in open source software distribution, has surpassed $2 billion sales a year.

One of the most innovative ideas in the industry is the implementation of the open source model in the semiconductor industry. The man standing behind this idea is GPS systems producer Trimble’s open source architect. He envisions small teams of engineers, most probably from academia, purchasing old production equipment, enhancing it thus creating a low cost production environment in the micro-fab style.

This cheap and available equipment will be utilized with free development tools and free libraries of intellectual property. The new technology might not be as advanced as that of the giant production corporations, “but if it will be good enough, it will enable very small groups of people to supply the market with new products, unhindered by the massive costs plaguing the production dinosaurs today.”

At some level, the open source hardware is already exit: It is represented by the micro-controllers development platforms such as Arduino andRaspberry Pi, sold for $5, and the minute System on Modules computers developed by SolidRun from Israel.

Even Intel is open sourcing: recently it has launched the MinnoBoard board computer based on a 64-Bit Intel chip, running Linux, Android and Windows operating systems. Intel also supplies the TinkerForge platform, enabling companies to speedily develop (and sell) diverse micro-controllers applications.

New compuer architecture

Another course of action is the adoption of new computer architecture. Almost all the currently available semiconductors include a processor based on a commercial Instruction Set Architecture (ISA). These architectures requires heavy payments for royalties, proving too expensive for many.

To reduce the costs of current computer architecture, researchers from the University of California Berkeley developed a new open source ISA version dubbed RISC-V, capable of running very powerful processors, up to 128 Bit. This architecture is intended to run very powerful servers, cheap embedded systems and even IoT accessories which are very economical in their use of energy and processing resources.

The architecture is currently distributed freely using the Berkeley Software Distribution free license. The Idea is not confined to academia – recently, RISC-V Foundation has been formed as an Industry group dedicated to expand the use of free computer architecture. In January 2015, the association reported it receives funding from 16 leading companies, among them: HP, Google, Oracle, Microsemi, Lattice and many more.

A window of opportunity for programmable components

The use of programmable components is not new in the industry. For many years such components have enabled companies to put out new products on the market, or products is small quantities by using programmable devices called Field Programmable Gate Arrays. Yet, the FPGA market remained a marginal with approximately $5 billion annual sales.

GSA estimates that the market will push FPGA manufacturer to supply more flexible and cheaper platforms, which in turn will enable them to bring new products to the market without without the manufacturing costs. The big challenge will be to supply programmable components, priced for the emerging IoT market.

Intel’s life boat

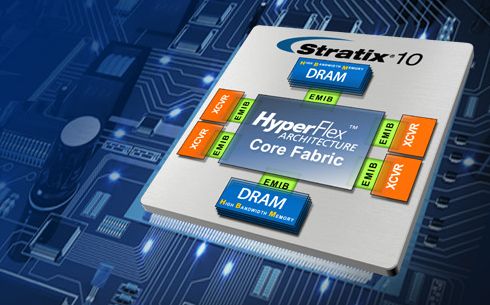

This analysis sheds new light on one of the most interesting a mega-deals of 2015: Intel acquisition of Altera for $16.7 billion. Altera is Xilix’s main competitor, and together they virtually dominate the global FPGA market.

Following the announcement of the deal, it was assumed that Intel is eager to harness Altera’s technology to produce extra powerful processors for data centers and server farms. In the last three years, many experiments conducted by the industry have proven that a combination of a CPU with FPGA drastically improves the performance of servers.

But the rationale behind the deal might be different, and much more far reaching: Intel is preparing a life boat to survive the future semiconductor industry, which will be dependent on the adaptation of new business models based on open source, open hardware and virtually zero costs. This idea explains the high price Intel agreed to pay. In fact, it was the biggest deal in Intel’s history.

Posted in: Featured Stories , News , Semiconductors , Technology