The board of directors of Texas Instruments has selected Brian Crutcher to become the company’s next president and chief executive officer (CEO). Crutcher will succeed Rich Templeton, who serves as president and CEO of TI for the last 14 years. The transition will be effective this June 1. Rich Templeton will remain the company’s chairman. The transition is a well-planned succession that follows Crutcher’s promotion to senior vice president in 2010, executive vice president in 2014, chief operating officer in 2017 and election to the board of directors last July.

Texas Instruments Incorporated (TI) is a global semiconductor design and manufacturing company that develops analog ICs and embedded processors. TI employs approximately 30,000 worldwide. It had total sales of $13.4 billion in 2016. Its market value in Nasdaq reached $115.1B. “This is an exciting time to lead TI,” said Crutcher. “Our semiconductors are inside tens of thousands of different types of electronics. I am energized by the opportunities we have ahead of us and look forward to working with TIers around the world to continue making TI a better supplier, employer and investment.”

Crutcher joined TI in 1996. Prior to his current role as executive vice president and chief operating officer of Texas Instruments, he served as TI’s executive vice president of Business Operations responsible for all TI’s businesses, sales and research and development. Throughout his career, he has held a number of leadership roles including senior vice president of TI’s Analog and DLP Products businesses, High Volume Analog and Logic, Power Management and Silicon Valley Analog and more. Early in his career, he served in a variety of leadership roles in the Sales and Applications organization throughout the U.S. He earned a Bachelor of Science in electrical engineering from the University of Central Florida (UCF) and a Master of Business Administration from the University of California, Irvine.

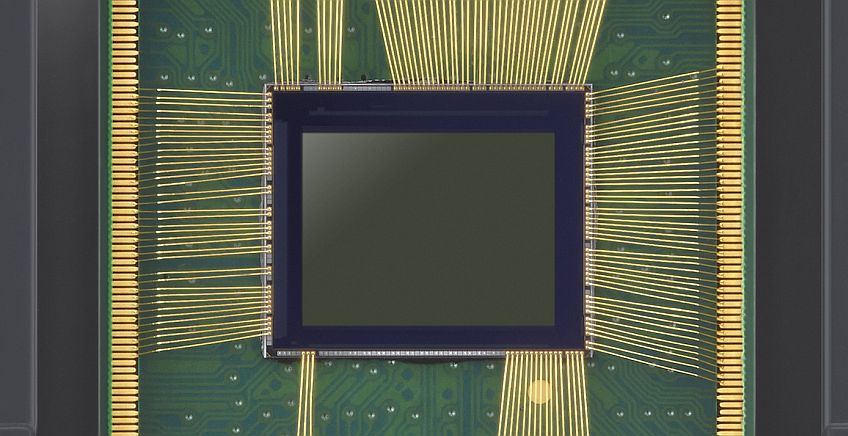

The image sensor market was valued at USD 14.19 Billion in 2017 and is projected to reach USD 24.80 Billion by 2023, growing at a CAGR of 9.75% between 2017 and 2023. According to a new research by Markets and Markets (Image Sensor Market by Technology) the major factors driving the growth include the increasing penetration of image sensors in automobiles, the trend of miniaturization and dual camera in smartphones and tablets, and the demand for improved medical imaging solutions.

The image sensor market for CMOS technology is expected to hold the largest share by 2023. CMOS image sensors are preferred over CCD sensors owing to small size, low power consumption, ease of integration, faster frame rate, and lower manufacturing cost. Advancement in the CMOS image sensor technology has improved the performance of image sensors, which have increased the penetration of the CMOS technology in consumer electronics.

3D Goes Faster

The 3D image sensor market is expected to grow at the highest CAGR during the forecast period. 3D image sensors find its application in fast-growing applications such as ADAS, machine vision, and computer vision. Another driver of 3D image sensors market is artificial intelligence in smartphones. Some companies, such as Apple, are already working on the inclusion of 3D image sensors in smartphones, and other manufacturers are expected to follow the same trend.

The market for non-visible spectrum (IR) is expected to grow at the fastest rate during the forecast period. It is gaining traction owing to its increasing use in automotive, medical, consumer electronics, and industrial applications. Images captured using low-megapixel cameras have numerous drawbacks. The image quality of such images gets reduced while zooming in, cropping, or taking prints. Hence, the demand for high-megapixel cameras is growing. To increase the number of pixels, manufacturers either have to increase the chip size or shrink the pixel pitch. However, a larger chip size would incur higher cost.

Consumers drive the Market

More than 80% of the demand for image sensors is from the consumer electronics application, which includes smartphones and tablets, cameras, computers, and wearable electronics. With the increasing penetration of dual camera in smartphones, the demand for image sensors is expected to increase. Automotive is another application that will contribute to the growth of the image sensor market. The development of advanced driver assistance system (ADAS) for automotive application is also expected to boost the demand for image sensors. It has been observed that with the development of ADAS, the number of cameras installed in a vehicle will be more than ten. This will create a huge demand for image sensors in automotive application.

VDOO from Tel Aviv has raised $13M in initial funding in a round led by 83North (formerly Greylock IL) and included participation by Dell Technology Capital and strategic individual investors, including David Strohm, Joe Tucci, and Victor Tsao. The funding will be used to develop and commercialize IoT security platform which provides an automated, end-to-end process that analyzes devices, delivers the right security requirements and implementation guidance for a full range of connected devices.

Loss of control of locks, alarms, video cameras, and many other connected things, can cause irreversible damage. The sheer number and diversity of connected devices, combined with evidence that attackers are building their infrastructure for future massive breaches, suggests that a significant number of users and businesses could be at risk. “An analysis of IoT attacks over the past 18 months, shows that even the simplest hacks can have serious consequences,” says Netanel Davidi, Co-CEO and founder at VDOO. “The problem is that there are no actionable processes or standards to guide IoT makers in the implementation of the proper security for each specific device.”

VDOO was founded by Netanel Davidi, Uri Alter, and Asaf Karas. Netanel Davidi and Uri Alter, Co-CEOs, previously founded Cyvera, a company that developed innovative endpoint security solutions, which was acquired by Palo Alto Networks in 2014. Asaf Karas is a cyber security researcher. In his recent role in the IDF, Asaf managed more than 100 cyber security experts.

Multi-stage Solution

VDOO has developed an end-to-end platform that allows IoT makers to quickly add the right level of security to their devices with minimal resources required. The foundation of VDOO’s solution is its comprehensive IoT Security Taxonomy engine that analyzes and then classifies tens of thousands of connected devices, to eventually determine the appropriate level of security for each, based on risk factors, threat landscape, and technology attributes.

“The Taxonomy engine combined with the automated analysis technologies enable, for the first time, the right, actionable security, for each and every analyzed product. Our goal is to balance security with device operation and the makers’ business considerations, so that requirements are specific to the device and reasonable at the same time,” says Uri Alter, Co-CEO and founder at VDOO. “Once the right requirements are determined, we make it easy and cost-effective for IoT makers to add security to their devices.”

The VDOO solution performs a security gap analysis on IoT devices, against the specific security requirements for each device type, and provides a detailed recommended plan of action to fill security gaps. Once security features have been implemented, VDOO validates that security requirements have been met and provides physical and digital certifications. The on-device digital certification agent monitors the security state of the device and communicates it to other systems such as gateways, firewalls, and edge solutions; which provides post-deployment security, ensuring the device is not being compromised.

“We believe that IoT security is critical for IoT growth and adoption across multiple industries. The ability to certify connected devices is a huge challenge and a key for IoT security,” says Yair Snir, GM, Dell Technologies Capital. VDOO is currently working with design partners on its initial release. An early beta program will be available to a broader group of beta customers in June 2018.

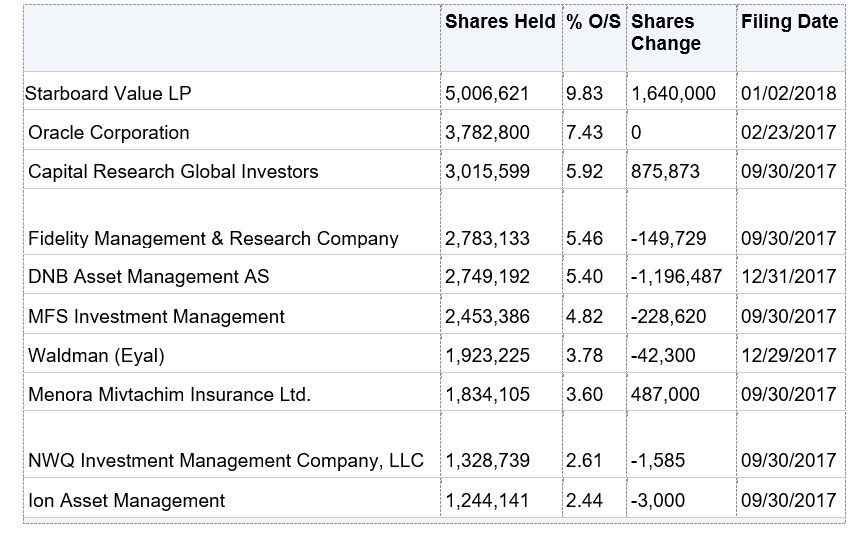

The biggest share holder of Mellanox Technologies, Starboard Value LP fro New York, ask the company’s shareholders to vote for its nominees during the coming 2018 Annual Meeting of Shareholders. This move came 10 days following an open letter that was sent to the CEO and Board, claiming Mellanox is one of the lowest operating margins of any fabless semiconductor company of reasonable scale. “The Company dramatically underperformed the peer group and the broader semiconductor industry over the past 1, 3 and 5 years.”

This letter has turned out to be just a warning sign. The actual move came this week when Starboard presented a list of nine candidates for election to the Board of Directors at the Company’s 2018 Annual Meeting of Shareholders. Since Mellanox’ board consists of nine members, it means that Starboard is looking for a complete control over the company. Among them Peter Feld, the Managing Member and founder of Starboard and current member of the Board of Marvell Technology Group.

Approximately 12 hours later, Mellanox published its results of Q4 2017: Revenues were $237.6 million in the fourth quarter, and $863.9 million in fiscal year 2017. GAAP gross margins were 64.1 percent in the fourth quarter, and 65.2 percent in fiscal year 2017. The company projects Revenues of $970 million to $990 million in 2018 with gross margins of 68.0 percent to 69.0 percent.

“We are pleased to achieve record quarterly and full year revenues,” said Eyal Waldman, President and CEO of Mellanox Technologies. “2017 represented a year of investment and product transitions for Mellanox. Fourth quarter Ethernet revenues increased 11 percent sequentially, due to expanding customer adoption of our 25 gigabit per second and above Ethernet products across all geographies. For the full fiscal 2017, our revenues from the high performance computing market grew 13 percent year over year.”

Is it enough for Starboard? Probabely not, but these results may help Mellanox to win the hearts of its shareholders.

The 10 Major Shareholders of Mellanox Technologies

Rohde & Schwarz is expanding its oscilloscope portfolio with the R&S RTM3000 and R&S RTA4000 series. Their 10-bit vertical resolution enables power measurements fulfilling the more stringent requirements demanded by advanced electronics. The R&S RTA4000, which is also ideal for analyzing serial protocols, even offers an acquisition memory depth up to 1 Gsample.

The new R&S RTM3000 oscilloscope offers bandwidths of 100 MHz, 200 MHz, 350 MHz, 500 MHz and 1 GHz. The products incorporate a proprietary 5 Gsample/s 10-bit ADC, and each model includes 40 Msample (80 Msample interleaved) per channel acquisition memory with an optional 400 Msample segmented acquisition memory. The new R&S RTA4000 oscilloscope offers bandwidths of 200 MHz, 350 MHz, 500 MHz and 1 GHz. These models include the same 10-bit ADC, but have even more memory, with an astonishing 100 Msample (200 Msample interleaved) per channel acquisition memory and standard 1 Gsample (1,000 Msample) segmented acquisition memory. Both instrument series feature a brilliant 10.1″ capacitive touchscreen display to operate quickly and efficiently.

10-bit vertical resolution

Power measurements, such as ripple and noise measurements of a DC line, demand an oscilloscope with high vertical resolution, low noise and excellent DC gain linearity. For most of the last three decades, oscilloscopes have predominantly offered 8 bits of vertical resolution, which allows a signal to be mapped to one of 256 vertical positions. The 10-bit ADCs of the R&S RTM3000 and R&S RTA4000 series support 1024 vertical positions. This is four times better than the common 8-bit oscilloscopes in this segment and essential for ripple and noise measurements. Both oscilloscope series provide extremely low signal noise, while the R&S RTA4000 series also offers class-leading signal integrity characteristics such as a DC gain accuracy down to 1 %.

Memory Depth for Serial Protocol Analysis

After bandwidth and sample rate, memory depth is the most important attribute that determines the instrument’s ability to handle a large range of troubleshooting tasks. Additional acquisition memory gives users longer time captures for testing and troubleshooting. This is especially true when analyzing serial communications or power on and off sequences. The R&S RTM3000 series oscilloscopes have eight to 20 times more memory than leading instruments from other manufacturers in this class. With 1 Gsample segmented memory, the R&S RTA4000 series has 200 times more memory than other oscilloscopes in its class that offer segmented memory.

For more information in Israel, contact Eastronics

Does the future of the Autonomous driving is certain? According to Autotalks from Kfar Neter, Israel, it is the regulation that can block the coming revolution. “Lack of coordination between autonomous vehicles and manned vehicles can fail the driverless car vision”, said Hagai Zyss, CEO of Autotalks, which specializes in semiconductors solutions of DSRC (Dedicated Short Range Communication) and V2X (Vehicle-to-Everything) technology.

“The problem of coordinating autonomous and manned vehicles must deeply concern policy makers and the auto industry. Decision makers must promote automotive technologies that will prevent accidents and save lives. The resolution of the coordination issue will be one of the key challenges of the industry in the next few years”. He believes that many people in the industry leap in their imagination to the point in time when all vehicles on roads will be autonomous, “but not everyone pays attention to the massive challenges in the long transition period, in which most of the vehicles will be manned and we will have to share our roads with autonomous vehicles.”

The Regulator must Step-in

Zyss: “Two key themes can demonstrate the problematic aspect of coordination: The first is the fact that accidents between autonomous vehicles and manned vehicles have already happened. Secondly, there is an inherent difficulty of human drivers to understand autonomous vehicles and vice versa. Beyond the fact that human drivers get stressed when they see an autonomous vehicle, they might make sudden lane changes, presume right of way or run red lights in a way that makes it difficult for autonomous vehicles to expect and respond to.

The solution, he said, may come by using DSRC-based V2X solutions to solve the issue of harmonizing autonomous and manned vehicles. “It is important to lay down an infrastructure of legislation and regulation that together with technologies, will ensure that the integration of autonomous vehicles into our roads will prevent accidents rather than cause accidents.”

Last year, Autotalks announced a $40 million financing round, led by Toyota’s investment arm Mirai Creation Investment Fund. In late 2016, the Japanese electronics giant DENSO decided to incorporate Autotalks’ chipset into the V2X platform it provides to car manufacturers. Autotalks is cooperating with several key players in the automotive industry such as Bosch, with whom it is carrying out a joint project to develop a motorcycle accident prevention communications technology (Bike-to-Vehicle – B2V).

A large proliferation of digital beamforming phased array technology has emerged in recent years. The technology has been spawned by both military and commercial applications, along with the rapid advancements in RF integration at the component level. Although there is a lot of discussion of massive MIMO and automotive radar, it should not be forgotten that most of the recent radar development and beamforming R&D has been in the defense industry, and it is now being adapted for commercial applications.

While phased array and beamforming moved from R&D efforts to reality in the 2000s, a new wave of defense focused arrays are now expected, enabled by industrial technology offering solutions that were previously cost prohibitive. In classical phased arrays, the analog beamforming subsystem combines all the elements to centralized receiver channels. Every element in digital beamforming phased array has waveform generators and receivers behind every front-end module, and the analog beamforming layer is eliminated. In many systems today, some level of analog beamforming is common.

The waveform generator and receiver channels serve to convert digital data to the operating band RF frequencies. Digital beamforming is accomplished by first equalizing the channels, then applying phase shifts and amplitude weights to the ADC data, followed by a summation of the ADC data across the array. Many beams can be formed simultaneously, limited only by digital processing capability.

Analog Devices has solutions for every section of a beamforming system illustrated, and for both analog and digital beamforming architectures.

Analog vs. Digital Beamforming

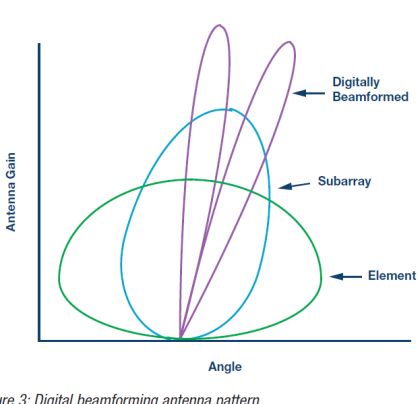

Digital beamforming antenna pattern

The objective of a digital beamforming phased array is the simultaneous generation of many antenna patterns for a single set of receiver data. The Figure (right) shows the antenna patterns at an element, the combined elements in a subarray, and the beamformed data at the antenna level. The primary obstacle of the subarrayed approach is that beamformed data must be within the pattern of the subarray. With a single subarray, simultaneous patterns cannot be generated at widely different angles. It would be desirable to eliminate the analog beamformer and produce only digital beamforming system. With today’s technology, this is now possible at L- and S-band. At higher frequencies, size and power constraints often necessitate some level of analog beamforming.

Beamforming goes Digital

However, the quest remains to approach near elemental digital beamforming, which places significant demands on the waveform generators and receivers. While the beamforming challenges place demands on the waveform generators and receivers to reduce size and power, there is a simultaneous demand to increase bandwidth for most system applications.

These objectives work against each other, as increased bandwidth typically requires additional current and additional circuit complexity. Digital beamforming relies on the coherent addition of the distributed waveform generator and receiver channels. This places additional challenges on both synchronization of the many channels and system allocations of noise contributions.

New Technologies Needed

The superheterodyne approach, which has been around for a 100 years now, provides exceptional performance. Unfortunately, it is also the most complicated. It typically requires the most power and the largest physical footprint relative to the available bandwidth, and frequency planning can be quite challenging at large fractional bandwidths. The direct sampling approach has long been sought after, the obstacles being operating the converters at speeds commensurate with direct RF sampling and achieving large input bandwidth.

Today, converters are available for direct sampling in higher Nyquist bands at both L- and S-band. In addition, advances are continuing with C-band sampling soon to be practical, and X-band sampling to follow. Direct conversion architectures provide the most efficient use of the data converter bandwidth. The data converters operate in the first Nyquist, where performance is optimum and low-pass filtering is easier. The two data converters work together sampling I/Q signals, thus increasing the user bandwidth without the challenges of interleaving.

The dominant challenge that has plagued the direct conversion architecture for years has been to maintain I/Q balance for acceptable levels of image rejection, LO leakage, and DC offsets. In recent years, the advanced integration of the entire direct conversion signal chain, combined with digital calibrations, has overcome these challenges, and the direct conversion architecture is well positioned to be a very practical approach in many systems. The future will bring increased bandwidth and lower power, while maintaining high levels of performance, and integrating complete signal chains in system on chips (SoC), or system in packages (SiP) solutions.

Digital Data Converter

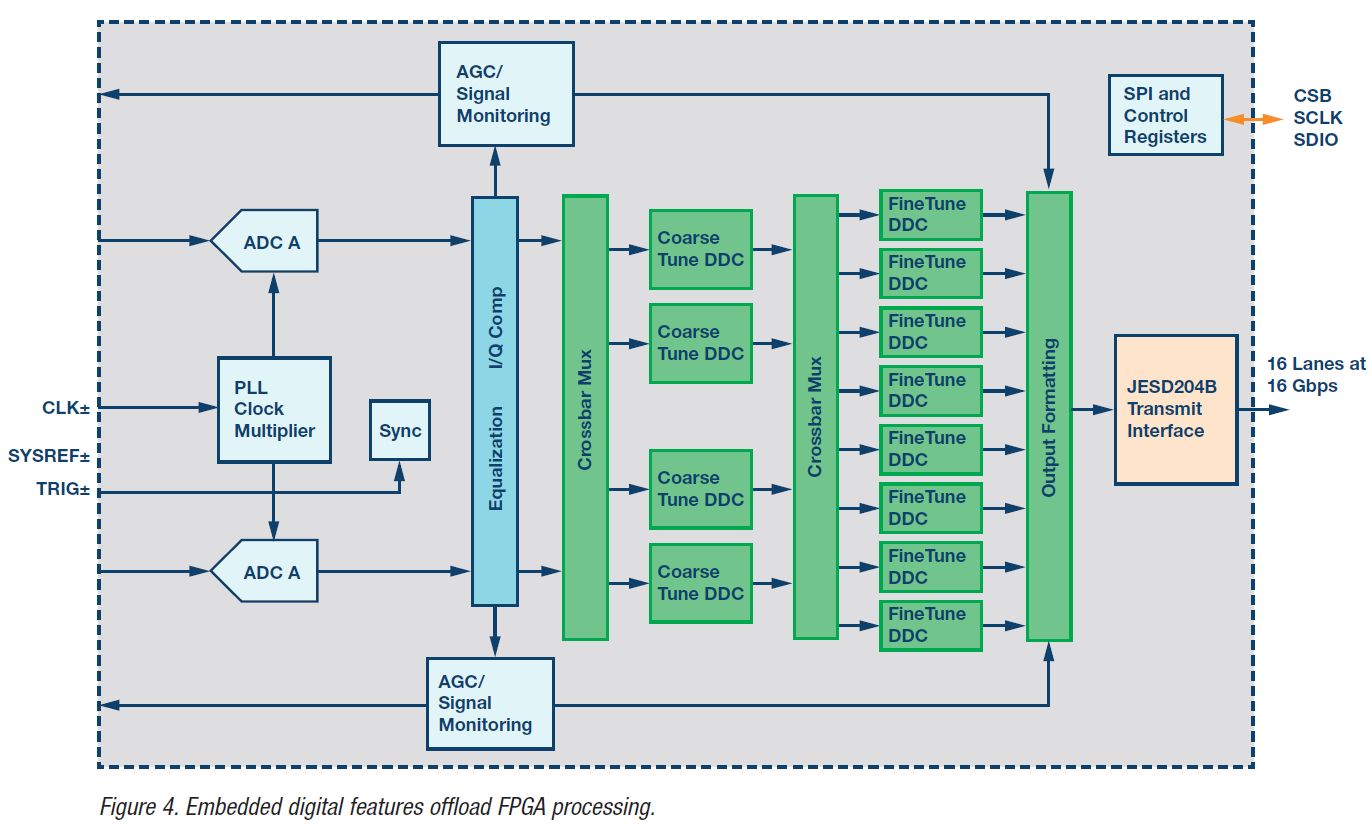

Data converter analog performance will continue to improve and these improvements at the analog level will include increased sampling rates for wider bandwidth, increased channel count, and maintaining the key performance metrics of noise, density, and linearity. These benefits will drive all of the RF signal chain solutions described, aiding new phased array solutions. An area of increased importance at the system level is the recent addition of many digital functions (as shown in the Figure below) that can be used to offload FPGA processing and help the overall system.

Embedded digital features offload FPGA processing

Recently released data converters include digital downconversion and filtering, which potentially reduces the data rate to the FPGA, reducing system power and FPGA processing requirements. Emerging Analog Devices data converters will continue to add functionality to the system, such as equalization and features at the front end of the digital beamforming processing.

Analog Beamforming

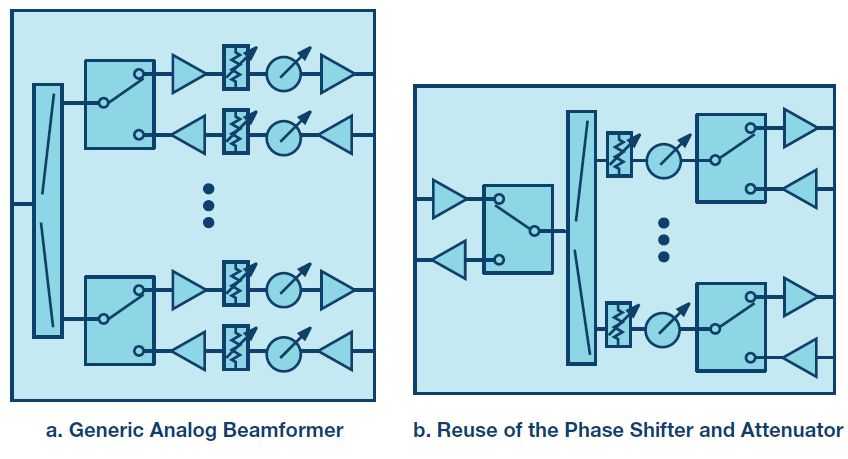

At high frequencies or low power systems, every element is challenged by size and power requirements. The use of analog beamforming reduces the number of waveform generators and receiver channels required to be digitized. Analog beamforming of phased array antennae is accomplished by adjusting the phase of the signal in the individual elements to steer the direction of the radiation pattern or beam.

Figure a below shows a generic analog beamforming example. Phase shifters are provided on both transmit/receive for beam steering, and many elements are combined to a single output. Figure b shows a functionally equivalent example where the phase shifter and attenuator are common to both the transmitter and receiver path enabled by microwave switches. The later topology reduces the number of phase shifters and attenuators required, but may require more frequent command updates to the devices.

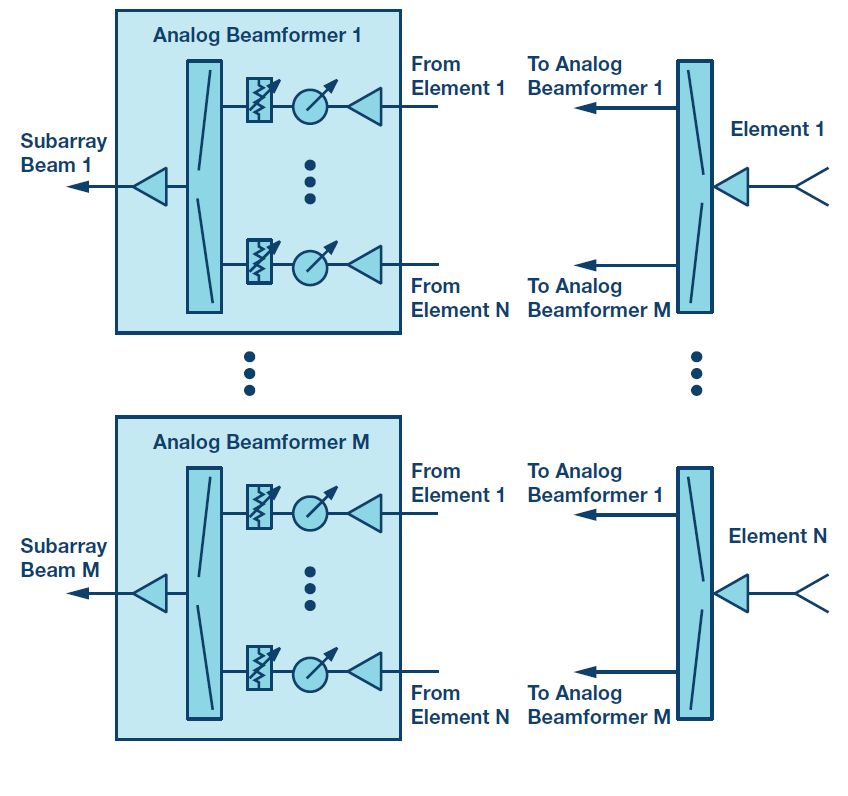

To overcome the constraints of a single subarray, multiple subarrays can be produced with a topology, such as shown in the Figure below. In this topology the low noise amplifier (LNA) outputs are split to many analog beamformers where N number of elements can produce M number of analog subarray beams. Each analog beamformer is programmed for a different antenna pattern. By repeating this topology across an array, digitally beamformed patterns can be created at widely disparate angles. This topology is one type of hybrid architecture that can provide the benefits of every element in the digital system, but with a reduced waveform generator and receiver count. The trade-off in this case is the analog beamformer complexity.

multi-subarrayed analog beamforming architecture

Traditional analog beamformers would have required a single function GaAs phase shifter and single function GaAs attenuator for each antenna element. More advanced approaches integrate the phase shifter and attenuator into a single GaAs front-end IC, that includes the power amplifier (PA), LNA, and switch. Analog Devices integrated analog beamformer chips achieve significant integration in SiGe BiCMOS technology, that incorporate four channels into a single IC with a reduced footprint, and less power dissipation.

Front-End Modules

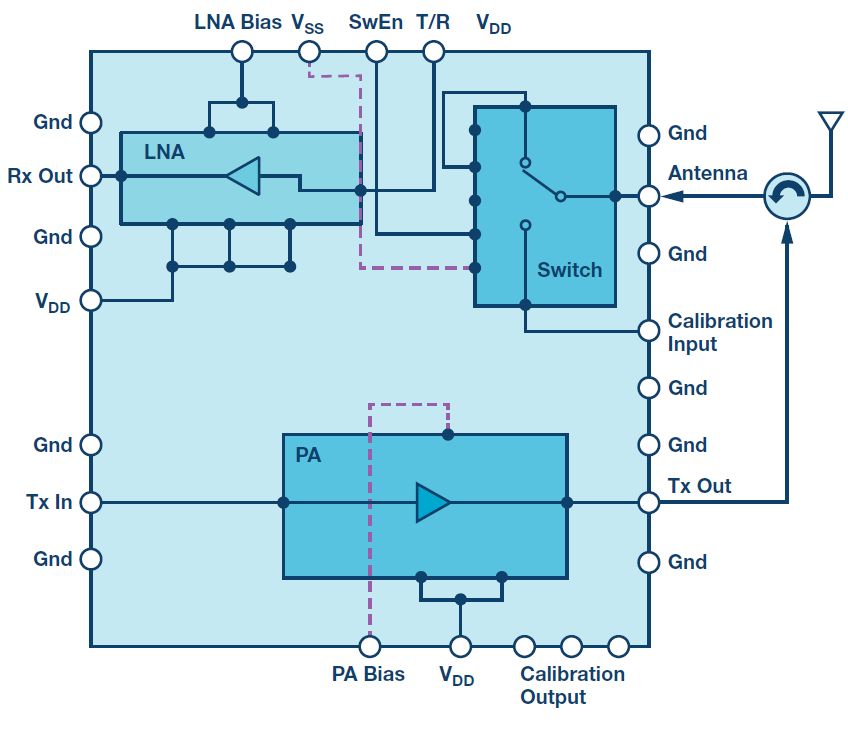

The front-end modules, sometimes called transmit/receive (T/R) modules, provide the interface to the antenna element. The front-end module is critical in terms of transmit power and efficiency, as well as receiver noise. The high power amplifiers (HPA) set the output power. The LNA establishes the system noise performance. Many systems require provisions for calibration or additional filters, and an example front-end module block diagram is shown below.

Example of front-end module block diagram

Summary

Digital beamforming phased arrays are now common, and rapid proliferation is expected with a huge range of frequencies and architectures being developed from L-band through to W-band. Analog Devices is enabling new system developments with SiGe beamformers, microwave frequency conversion, front-end modules, and high speed converters. Our beamforming solutions combined with our power amplifiers, low noise amplifiers, and switch technologys.

We use cookies to personalize content and ads, to provide social media features and to analyze our traffic. We also share anonymous information about your use of our site with our social media, advertising and analytics partners. View more

What personal data we collect and why we collect it

We collect anonymous data on visitors in this website for business purposes such as enhancing user experience, digital marketing and search engine optimization.

We collect personal data such as email address and names on various forms - all forms present in this website include consent checkboxes and clear reason for collecting the data: general inquiries on our products, newsletter subscription, professional inquiries job applications. All forms are designed in accordance with GDPR requirements.

Comments

When visitors leave comments on the site we collect the data shown in the comments form, and also the visitor’s IP address and browser user agent string to help spam detection.

An anonymized string created from your email address (also called a hash) may be provided to the Gravatar service to see if you are using it. The Gravatar service privacy policy is available here: https://automattic.com/privacy/. After approval of your comment, your profile picture is visible to the public in the context of your comment.

Media

If you upload images to the website, you should avoid uploading images with embedded location data (EXIF GPS) included. Visitors to the website can download and extract any location data from images on the website.

Contact forms and newsletter

We use Gravity Forms as our platform of choice for all forms present in this website. Forms present in this website have been modified to fit GDPR requirements.

Unless specifically specified and approved by visitor, we do not use the collected data for marketing purposes.

We use Mailchimp to collect email addresses and send periodical marketing materials to our customers.

Handling and management of all email addresses and mailing operations is conducted under GDPR terms and guidelines provided by Mailchimp.

All subscribers are able to change their subscriptions preferences or unsubscribe at any given time.

Techtime has accepted the Data Processing Addendum agreement provided by Mailchimp for all its Mailchimp accounts.

All our lead collection forms have been altered in accordance with GDPR requirements and now include unchecked checkboxes in order to accept the explicit consent of the user prior to form submission.

Cookies

If you leave a comment on our site you may opt-in to saving your name, email address and website in cookies. These are for your convenience so that you do not have to fill in your details again when you leave another comment. These cookies will last for one year.

If you have an account and you log in to this site, we will set a temporary cookie to determine if your browser accepts cookies. This cookie contains no personal data and is discarded when you close your browser.

When you log in, we will also set up several cookies to save your login information and your screen display choices. Login cookies last for two days, and screen options cookies last for a year. If you select "Remember Me", your login will persist for two weeks. If you log out of your account, the login cookies will be removed.

If you edit or publish an article, an additional cookie will be saved in your browser. This cookie includes no personal data and simply indicates the post ID of the article you just edited. It expires after 1 day.

Embedded content from other websites

Articles on this site may include embedded content (e.g. videos, images, articles, etc.). Embedded content from other websites behaves in the exact same way as if the visitor has visited the other website.

These websites may collect data about you, use cookies, embed additional third-party tracking, and monitor your interaction with that embedded content, including tracing your interaction with the embedded content if you have an account and are logged in to that website.

Analytics

We use Google Analytics regularly for monitoring user behavior and traffic sources and utilize the gathered information for enhancing user experience and for business purposes.

The use of Google Analytics in done according to GDPR terms and guidelines provided by Google.

Legal Entity: Techtime.

Primary Contact (a.k.a. "Notification Email Address"): roni@techtime.co.il - this email is designated for receiving notices under the Google Ads Data Processing Terms.

Who we share your data with

We use various cloud platforms and third party providers for the purpose of operating this website.

We do not share or sell your data for any commercial purpose other than specified above.

We use the following processors for the operating this website and executing related digital marketing campaigns:

WP Engine - Hosting Provider

Cloudflare - Cloud based security and web performance processor.

Google Cloud Platform - data centers provider for WP Engine

Sucuri - Website security provider

Mailchimp - Newsletter service provider

Google Analytics, Adwords, Webmasters

Facebook - We use Facebook for advertising and place tracking code on our website for enhancing digital marketing campaigns (i.e - Facebook Pixel).

Planwize Ltd - Digital Marketing Agency.

How long we retain your data

If you leave a comment, the comment and its metadata are retained indefinitely. This is so we can recognize and approve any follow-up comments automatically instead of holding them in a moderation queue.

For users that register on our website (if any), we also store the personal information they provide in their user profile. All users can see, edit, or delete their personal information at any time (except they cannot change their username). Website administrators can also see and edit that information.

What rights you have over your data

If you have an account on this site, or have left comments, you can request to receive an exported file of the personal data we hold about you, including any data you have provided to us. You can also request that we anonymize or erase any personal data we hold about you. This does not include any data we are obliged to keep for administrative, legal, or security purposes.

Request for Receiving Data Associated with One’s Email Address

Users may request to receive access to all related information submitted to this website for their review.

In accordance with GDPR compliance, user may further request the anonymization of such data.

In order to request access for all data associated with a given email address, users may submit the request here. Users then receive an email with a link to a page with all related information.

The link is valid for 24 hours. Users may submit additional request for the same email address once in every 24 hours.

A request for anonymization should be sent separately: User may select the data he or she wishes the site owner to anonymize so it cannot be linked to his or her email address any longer. An email confirmation will be sent once linked data has been successfully anonymized.

Where we send your data

Visitor comments may be checked through an automated spam detection service. All our processors and third party providers comply with GDPR requirements and apply privacy by design and necessary measure to ensure that personal data is being processed and handled in accordance with requirements. The list of our third party service providers and processors is listed above.

Contact information

For all privacy-specific concerns inquiries, you may contact us at mail@mail.com

How we protect your data

We use rigorous practices in order to protect our website and data collected, as well as world class cloud and hosting providers.

Communication between visitor and the server is encrypted using SSL.

The site is protected with web application firewall and is undergoing daily security scans, regular software updates by a dedicated team in order to minimize the risk of data breach.

What data breach procedures we have in place

Once a data breach is detected, our providers execute a dedicated standard operational procedure in order to assess the scope and potential damage, provide immediate remedy, patch any potential security holes and notify users who may be affected by the breach.

We may contact affected users with one or more form of communication within 72 hours and provide the needed information as to the scope of the data breach and actions taken.

What third parties we receive data from

We do not receive data from third parties for our marketing campaigns.

What automated decision making and/or profiling we do with user data

We may apply remarketing/retargeting methods while conducting online advertising using Google Facebook and the likes.

The above is conducted by applying various tracking codes into our website in order to track and retarget users based on

By visiting and using this website you are hereby provide your consent for the use of the above means and methods.