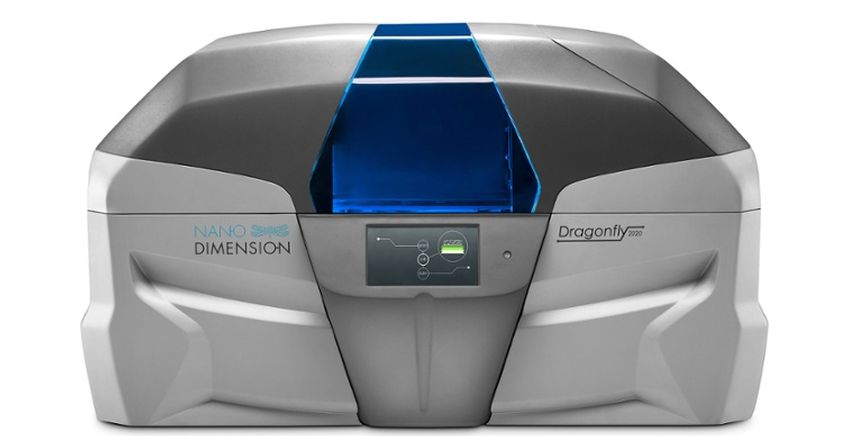

Years of development, cooperation’s and business contacts build up have finally calumniated into a first commercial tryout for Nes Ziona, Israel based 3D PCB printer developer Nano Dimensions. The company has announced it has supllied its Dragonfly 2020 printer to a renowned Israeli defense company. The printer will undergo a series of test in order to test if it complies with the strict standards maintained by the unnamed Israeli high-tech defense company. Nano dimension’s stock has gained 3.75% following the announcement.

The first commercial bete is of crucial importance for the Israeli PCB printer developer. Until now, the Dragonfly 2020 has only been tested in laboratory conditions. The product is not yet commercially distributed, and a successful deployment of the printer by a leading company could be an enormous achievement for Nanao dimensions, opening the door for large scale commercial distribution. In its announcement, the company has defined the deployment of the printer as a pilot, aimed to asses costs and functionality, a step towards upcoming commercial distribution.

A positive feedback will undoubtedly help the company to find further interested customers. Furthermore, the fact that a major company deems the product ripe for testing is a major vote of confidence in the Nano’s technology. “Today, only two years since our first fundraising and since our shares began trading on the TASE, we mark this important milestone of supplying our first system to a beta partner, enabling them to print multilayer electric circuits in several hours,” said Amit Dror, CEO of Nano Dimension. “We look forward to completing production of more printers destined for additional partners and customers in Israel and around the world.”

A leading innovator in 3D printing Arena

Nano Dimensions developed the Dragonfly, a 3D printer enabling the use of advanced nanoparticle conductive and dielectric inks for rapid prototyping of complex multilayer printed circuit boards (PCBs). The process is based on the use of polymeric materials to create insulating layers, and conductive silver ink for the electrical conductors.

Founded in 2012, Nano Dimension has a strong position in the emerging market of PCB 3D printing. Last month, the company and San Francisco based Fathom announced a collaboration on introduction of Nano Dimension’s Dragonfly 3D printer to the US. West cost – the very heart of American High-Tech industry.

The kit will combine Mobileye’s sensing and mapping systems with Delphi’s driving software algorithms. The kit is scheduled for release as soon as 2019. Mobileye’s stock surged by more than 8% following the announcement

Israeli Mobileye and Delphi, one of the world’s leading automotive electronic components manufacturer, announced a strategic cooperation in the development of fully autonomous driving system. The system to be developed by the two companies is planned as a kit, which could be installed on any car,thus saving the need to develop a fully autonomous car from scratch. The system will be unveiled early in 2017 at the CES exhibition. Mobileye and Delphi intend to distribute it by 2019.

The concept presented by the two companies is similar to American Otto – a company producing autonomy kits for truck. Otto has just been acquired by UBER (see our featured story) for $680 million. While the leading auto manufacturers such as Ford, Volkswagen, Tesla and others are building cooperation’s with technology providers and designing their unique autonomous vehicle models, Mobileye and Delphi’s kits are aimed at middle scale and small scale manufacturers, who can’t join the race to autonomy by themselves.

Mobileye and Delphi’s system aims to provide a “shelf system” which could be used by a wide veraiety of automotive manufacturers, wishing to “autonomize” their models. While the system is scheduled for distribution as soon as 2019, it is important to remember that the integration of the system takes some two years, so this early date is somewhat misleading, and does not constitute a break with “traditional” autonomy schedules.

The automated driving solution will be based on key technologies from each company. These include Mobileye’s EyeQ® 4/5 System on a Chip (SoC) with sensor signal processing, fusion, world view generation and Road Experience Management (REM™) system, which will be used for real time mapping and vehicle localization. Delphi will incorporate automated driving software algorithms from its Ottomatika acquisition, which include the Path and Motion Planning features, and Delphi’s Multi Domain Controller (MDC) with the full camera, radar and LiDAR suite.

Automatic negotiations

In addition to each company’s “dowry”, teams from both companies will develop the next generation of sensor fusion technology as well as the next generation human-like “driving policy.” This module combines Ottomatika’s driving behavior modeling with Mobileye’s deep reinforcement learning in order to yield driving capabilities necessary for negotiating with other human drivers and pedestrians in complex urban scenes.

“The Mobileye and Delphi relationship started in 2002 with the implementation of what was one of the most advanced active safety systems of the time. Our long history together is key to the success of this ambitious endeavor,” said Professor Amnon Shashua, Mobileye Chairman and Chief Technology Officer. “Our partnership with Delphi will accelerate the time to market and enable customers to adopt Level 4/5 automation without the need for huge capital investments, thereby creating a formidable advantage for them.”

Kevin Clark, Delphi President and Chief Executive Officer added that “This partnership will allow us to give our customers an increased level of automated capabilities faster and more cost effectively. The collective expertise of our two organizations will accelerate the creation of new approaches and capabilities that would likely not have been possible working alone. This is a win-win for both companies and our customers.”

Following the joint announcement made by the two companies, Mobileye’s stock surged by up to 8%, crossing the $10 billion market cap mark.

Working to maintain security during the 2016 Rio Olympics, police forces in Brazil are using an armored vehicle made by Plasan. The vehicle are equipped with fire detection and surpression systems by yet another Israeli company – Sectrex

Plasan’s Guarder armored vehicle helping to secure the 2016 Rio Olympics (Plasan)

Now that the Olympic Games have come to a successful conclusion, it is easy to forget just how worried everybody was just a few weeks ago. Many experts warned of the dangers of a terror attack or large scale civilian unrest in Rio. The Brazilian police did not take these treats lightly, and carried out unprecedented security effort during the games, which helped the festivities run smoothly and securely. During the operation, Brazilian police forces made use of an advanced Israeli made armored personal carrier (APC), Palsan’s “Guarder”.

The 4×4 vehicle can carry a payload of up to 3,500 kilograms in a spacious composite-steel hull with STANAG 3 armored protection. In Brazil, the Guarder is currently being used by the special weapons and tactics team (SWAT) of the police department of Sao Paolo. The “Guarder” makes it possible for a driver, commander and 22 fully-equipped troops to quickly and safely traverse any terrain. Sao Paolo police officers report that the vehicles are typically used for large-scale policing and rescue operations. It was mentioned that officers appreciate the ability of the vehicle’s strong cameras, which can capture optical and thermal images, which provide better information to the commanders. Above all, the vehicle provides more security, both for the operators and for the public, who feel more secure in the presence of the huge vehicle.

“We’re proud to see our vehicle used by police forces in Brazil as they work to keep the Rio Olympics safe and secure,” saidDani Ziv, CEO of Plasan. “From the beginning, we knew that the Guarder is the perfect armored vehicle for this mission. We’re all honored to be participating, in this way, in the Rio Olympics, helping to keep the peace at this amazing event.”

A state of the art fire extinguishing system by Spectrex

Palsan’s “Guarder” is equipped with the SAFE automatic fire detection and suppression system by Israeli Spectrex. The system deploys advanced optical detectors, providing the fast response time, high false alarm immunity, alongside homogeneous and efficient suppression agent dispersion, helping to protect security forces and their vehicles. Spectrex was recently sold to American engineering giant Emerson in a $99 million deal. The company’s patented optical UV/IR and IR3 Flame Detectors and SAFE systems are integrated in over 30,000 vehicles and are approved by US Army, NATO forces and other leading armies.

The DRAM market is forecasted to shrink by 19% in 2016, causing worldwide semiconductor market to shrink by 2%. In 2017, prices might recover

The plunge of the DRAM market continues to weigh heavy on the worldwide semiconductor market profitability in 2016. According to a current research by specialized semiconductor markets research company IC Insights, the DRAM market is forecasted to shirk by a staggering 19%. This extreme downward trend is caused by the drop in the price of DRAM as well as a shrinkage in global shipping’s.

The current downward trend is not new – it is actually going on for several months now. Declining shipments of desktop and notebook computers, the biggest users of DRAM, as well as declining tablet PC shipments and slowing growth of smartphone units have created excess inventory and suppliers have been forced to greatly reduce average selling prices in order to move parts. A DRAM ASP decline of 16% coupled with a forecast 3% decline in DRAM unit shipments is expected to result in the DRAM market declining 19% in 2016 (Figure 1), lowest among the 33 IC product categories IC Insights tracks in detail. This steep decline will be a drag on growth for the total memory market (-11%) and for the total IC market (-2%) in 2016.

Volatility in average selling price are not new to the DRAM market. Annual DRAM average selling price increases of 48% and 26% in 2013 and 2014 propelled the DRAM market to more than 30% growth each year. In fact, the DRAM market was the strongest growing IC product segment in each of those years. Then, marketshare grabs and excess inventory started the cycle of steep price cuts in the second half of 2015 and that continued through the first half of 2016.

IC Insights forecasts an improvement in the DRAM market by 2017. Nevertheless, this foretasted recovery may very well prove to be a short term trend – while demand for DRAM is expected to grow due to the rapid development of Big Data applications, as well as IoT and the mobile market, supply is about to explode as well. Only recently, several Chinese producers such as Sino King Technology and Fujian Jin Hua have announced they will be mass producing DRAM memories by 2017-18.

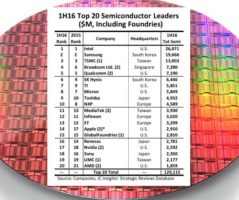

While the slight improvement in Q2 is good news, the 5.8% drop in sales in 2016 is still the harsh reality for worldwide Semiconductor industry. Meanwhile, industry giants live in a parallel universe: the 20 leading Semiconductor sales grew by 7%

Q2 earning reports season has passed, and now is a good time to take stock of the semiconductor industry’s results in the passing quarter. The semiconductor industry has drawn a great deal of attention in the last months due to weakening demand and grim growth outlooks for 2016.

According to Semiconductor Industry Association (SIA), worldwide sales of semiconductors reached $79.1 billion during the second quarter of 2016, an increase of 1.0 percent over the previous quarter. Yet a comparison to the same quarter last year reveals the true width of the industry’s crisis: Q2 2016 represent a 5.8% decrease in semiconductor sales compared to the second quarter of 2015.

The main causes for this year’s slump are the ongoing slump in the global economy’s growth – mostly in Europe and China, the sharp decline in DRAM and NAND memory markets, and the weakening of PC and mobile markets.

Grim forecasts for 2016

The outlook for the second half 2016 is far from rosy. According to World Semiconductor Trading Statistics (WSTS), worldwide semiconductor market is forecasted to be $327 billion in 2016, a 2% decrease from 2015.

Some sectors of the worldwide semiconductor market grew in Q2 2016, but the growth of sectors such as Optoelectronics (1.8%), Sensors (7.6%), and Analog ICs (1.0%) is expected to be offset by declines in

Memory (-10.2%) and Logic (-2.5%). While the forecasts for 2016 remain grim, there is a light in the end of the tunnel – according to WSTS, growth is expected to commence in 2017 and 2018. For 2017 and 2018, all major product categories and all regions are forecasted to grow reaching US$341 billion in 2018. As a result, the worldwide semiconductor market is forecasted to be up ~2% year-on-year in both 2017 and 2018.

what crisis? The top-20 are booming

The 20 industry leaders grew by 7%

A further current research sheds another light on current semiconductor industry trends: IC Insights, a research company specializing in the semiconductor industry has published a report on the top-20 semiconductor supplier’s sales in 2016. The Reports shows that the sales of these 20 industry leaders have risen by 7% compared to the first quarter of this year.

From the top-20 supplier’s, 7 reported a double-digit increase in sales, while only two reported a decrease in sales: Intel (-1%) and Japanese Renesas (-3%). The company reporting the highest growth rate was Taiwanese MediaTek with a staggering 32% increase in sales, mainly due to a large volume of processors sold to Chinese mobile manufacturers such as OppO and Vivo. Intel, Samsung and TSMC remain firm on the top of the list.

Otto’s acquisition by Uber for $680 million teaches that the autonomous car revolution is focused on autonomy, not on cars: Branding, added value and most of all profits will shift from automotive hardware manufacturers to the new autonomy service providers

Roni Lifshits, Editor of Techtime News

Last week, Uber founder and CEO Travis Kalanick announced the acquisition of San Francisco based Otto, for an estimated sum of $680 million. This acquisition is an amazing achievement considering that Otto was founded in February 2016, an infant startup by any account. An examination of the deal, and of Uber’s strategy suggests that behind this deal lies a long term strategy, focused on autonomous transportation business models rather than groundbreaking autonomous driving technology.

Otto co-founder Roni Lior

Otto was founded by to ex Google engineers: Israeli Lior Ron, former head of Google Maps development section and Anthony Lewandowsky, former leader of google’s self-driving car project. As early as 2004, Lewandowsky was among the developers of the Gohstrider – an autonomous motocycle developed for the Defense Advanced Research Projects Agency (DARPA). In his announcement, Kalanick disclosed that all 90 Otto employees will join Uber following the acquisition.

Using truck to bypass obstacles

Uber and Otto’s actions in the autonomous driving field are surprising and thought provoking. Otto has decided to bypass most of the difficulties bundled with the development of autonomous vehicles, focusing on trucks hauling goods on America’s highways. Otto does not develop and manufacture trucks – it develops and orientation and control kits that can be mounted onto exiting trucks, making these autonomous. Last month, Otto fitted three old Volvo Trucks with a sensor kit including a radar, a LiDAR system and several cameras. The trucks were that launched to roam Navad’s higways driverless.

This strategic decision has several advantages: Long-haul transit accounts to 70% of American cargo traffic, and suffers from a severe shortage in drivers. On the other hand, Highways pose a much simpler challenge for autonomous driving than urban surroundings, in which most companies such as Tesla and Google are focusing.

Long-haul fleets also have a business model that can absorb the additional costs associated with the installation of autonomous driving systems – even in massive numbers. The goal: to supply autonomous trucks by 2021, the year in which autonomous driving is almost unanimously believed to mature, technologically as well as legally. This model actually complies with Uber’s exiting autonomous driving strategy.

A cooperation with Volvo

In late 2015, Uber has established its autonomous driving section, luring most of Carnegie Mellon University’s robotics faculty. Uber’s move also bypassed the autonomous vehicle manufacture problem. Uber has signed a cooperation agreement with Volvo. Volvo was to supply Uber with XC90 cars, on which Uber was to install an autonomy kit, connected to Uber’s application – making these driverless cabs for Uber’s use.

These two moves make clear a crucial point – the autonomous driving revolution is focused on the autonomy, not on the car. The added value if an autonomous vehicle or an autonomous fleet are measured by the degree of autonomy. I.e. navigational systems, reliability, the servicing infrastructure provided by the cloud and so on. The branding will shift from car manufacturers to autonomy service providers.

For companies such as Uber, this is a golden orotundity. Exactly like Google is entering the autonomous driving arena in order to turn its mapping algorithms a new income source, and Amazon is entering the UAV markes in order to enhance its logistical capabilities, Uber has discovered that autonomous driving is opening up a new opportunity for its core business: mobility services.

What’s a “white car”?

The Otto acquisition shows that autonomous driving is creating new business models: through Otto, Uber can become a transportation company supplying service on demand, using an application. It’s similar to supplying new applications using exiting communication infrastructure. In fact, Uber even won’t have to purchase a single truck – it can offer transportation solution providers to install its autonomy kit and join Uber’s pool, thus securing work orders.

One of the interesting questions is the car manufacturer’s response to these developments. The trends led by companies such as Uber might force them to establish new service companies supplying autonomy services on demand. If traditional car manufacturers fail to do so, they face a real danger that in a few years, most of the cars will become “white boxes”: a standard shelf product, not unlike a PC or a server, sold according to its value, and not according to the brand’s added value.

China formed the High-end Chip Alliance: a group of 27 industry giants, universities and government offices which will lead a coordinated effort to establish an independent leading Semiconductor Industry

The establishment of a local semiconductor industry has been one of the Chinese government’s strategic goals over the last few years. The focused governmental effort begun as early as 2000, but the first attempts have not been successful. Last week, the Chinese efforts have geared up, with the formation of a Chinese High-end Chip Alliance. The alliance includes 27 companies and public organizations, forming a national concert of companies, funding agencies and research institutions.

The official proclamation of the alliance stated that it will focus on the development of processors, memories, sensors, FPGA components, DAC and ADC signal convertors and various other essential components for the establishment of a fully independent semiconductor industry.

The founding 27 members of this alliance include Tsinghua Unigroup, Yangtze River Storage Technology, Huawei, SMIC, ZTE and China Academy of Telecommunication Research (a branch of the country’s Ministry of Industry and Information Technology). Loongson Technology will coordinate the development of powerful processors for the alliance, while Tsinghua Unigroup, established by the Chinese government, will help finance the founding of a strong local semiconductor industry.

“This alliance of government, academia and industry aims to create a complete ecosystem for domestic semiconductor manufacturers”, said Jian-Hong Lin, research manager of TrendForce. “If successful, the alliance will create a chip industry chain starting from chip architecture to chip production, operation systems, devices, platforms and finally to the IT service market. In sum, this move is another indication of China’s ambition to transform itself from a major manufacturing country by export volume to a global manufacturing leader in terms of product quality.

A processor manufactured by Chinese Loonson

In a blog published in the company’s site, Lin explained that the Chinese move aims to elevate china from a mere producer of chips to a global industry leader. ““Taiwanese semiconductor companies cannot survive on just the demand from the domestic market and compatriot electronics brands. This is especially true for the local IC design houses. Their long-term growth will depend discovering new sources of demand and application needs in the international market. Still, China currently is the largest market and has the largest client base for Taiwanese IC design houses. Whether Taiwanese IC industry is allowed to form effective joint ventures or strategic partnerships with the Chinese counterpart is an issue that Taiwan’s government and technology enterprises need to address after the establishment of the high-end chip alliance in China.”

An efficient management of such a national alliance is not an easy task. For example, Tsinghua Unigroup subsidiary Spreadturn develops 16 nanometer chips, while Chinese chip production contractor SMIC has not yet acquired 16 nanometer geometry production capabilities. Nevertheless – the parties joined in the new alliance have shown in the past, that a continuous effort can help them to achieve impressive feats.

Loongson Technologies for example, demonstrates how a Chinese company can achieve a goal which only recently would have been perceived as impossible. The company was founded as part of the Chinese effort to develop a processor based on independent architecture for supercomputers. The company began its life as a project of the government owned ICT. The company has developed a uniquely robust CPU architecture of a 64 core processor, which is intended to grow to a thousand core one.

American mistake which built Chinese the industry

Loongson’s success is the result of an American mistake: during the nineties, Digital (acquired by Compaq, later acquired by HP) has developed a RISC architecture dubbed Alpha, which is still considered one of the best processor families in industry, providing 64 bit processing capabilities as soon as 1991. All this did not save the brand, which was “killed” by Digital and Compaq due to short term business considerations. The companies allowed Chinese acquire the unique technology.

Inside Smic’s Fab. source: ARM Connected Community

The Chinese chose this discarded architecture, due to the understanding that it saves them the enormous challenges of developing a new architecture fro scratch. In April 2012 they have been proven right: The ICT institute and Loongson Technologies produced a processor in the already than obsolete 65 nanometer geometry. Nevertheless, the processor had a calculation power matching these of concurrent Intel processors. In fact, the same processor was integrated into the Chinese inan Petaflop Shenwei supercomputer, which is considered more efficient in its use of energy than American counterparts.

Loongson’s processor was dubbed Godson – a worth remembering considering that Loongson will coordinate Chinese processor architecture development, and this will be based on the Godson processor.

Tsinghua’s ambitious goal

Another name worth remembering is that of major financing house Tsinghua Unigroup. In 2013 the chines government decided to make a long term investment in the local semiconductor industry. After a few failed attempts as early as 2000, the Chinese government tried a new strategy: instead of trying to develop new technologies, it would establish an independent investment fund which will pursue a strategy aimed to encourage local companies to merge in order to form semiconductor giants.

In September 2014, Intel has made a massive investment in Tsinghua Unigroup, acquiring 20% of its shares for some $1.5 billion. Intel said that the investment’s goal was to expand the use of Intel’s computing platform in the Chinese mobile market. The investment agreement has two very interesting features: Intel is interested in conducting Architecture research and joint projects in China. As well as to develop mobile communication solutions.

In July 2015, Tsinghua tried to acquire American memory components producer Micron, offering a staggering $23 billion. Micron is considered the world’s second largest memory component producer, and its sale to a Chinese group did not go through – probably due to active discomfort by US administration.

The failure of the attempt to take control of Micron does not seem to deter Tsinghua Unigroup from making further strategic investment outside china. In September 2015, Tingsghua Unigroup chairman Zhao Weigo told Reuters of his plans to invest $47 billion over the next five years to to build the world’s third-biggest chipmaker. No wonder the Taiwanese are feeling uneasy.

We use cookies to personalize content and ads, to provide social media features and to analyze our traffic. We also share anonymous information about your use of our site with our social media, advertising and analytics partners. View more

What personal data we collect and why we collect it

We collect anonymous data on visitors in this website for business purposes such as enhancing user experience, digital marketing and search engine optimization.

We collect personal data such as email address and names on various forms - all forms present in this website include consent checkboxes and clear reason for collecting the data: general inquiries on our products, newsletter subscription, professional inquiries job applications. All forms are designed in accordance with GDPR requirements.

Comments

When visitors leave comments on the site we collect the data shown in the comments form, and also the visitor’s IP address and browser user agent string to help spam detection.

An anonymized string created from your email address (also called a hash) may be provided to the Gravatar service to see if you are using it. The Gravatar service privacy policy is available here: https://automattic.com/privacy/. After approval of your comment, your profile picture is visible to the public in the context of your comment.

Media

If you upload images to the website, you should avoid uploading images with embedded location data (EXIF GPS) included. Visitors to the website can download and extract any location data from images on the website.

Contact forms and newsletter

We use Gravity Forms as our platform of choice for all forms present in this website. Forms present in this website have been modified to fit GDPR requirements.

Unless specifically specified and approved by visitor, we do not use the collected data for marketing purposes.

We use Mailchimp to collect email addresses and send periodical marketing materials to our customers.

Handling and management of all email addresses and mailing operations is conducted under GDPR terms and guidelines provided by Mailchimp.

All subscribers are able to change their subscriptions preferences or unsubscribe at any given time.

Techtime has accepted the Data Processing Addendum agreement provided by Mailchimp for all its Mailchimp accounts.

All our lead collection forms have been altered in accordance with GDPR requirements and now include unchecked checkboxes in order to accept the explicit consent of the user prior to form submission.

Cookies

If you leave a comment on our site you may opt-in to saving your name, email address and website in cookies. These are for your convenience so that you do not have to fill in your details again when you leave another comment. These cookies will last for one year.

If you have an account and you log in to this site, we will set a temporary cookie to determine if your browser accepts cookies. This cookie contains no personal data and is discarded when you close your browser.

When you log in, we will also set up several cookies to save your login information and your screen display choices. Login cookies last for two days, and screen options cookies last for a year. If you select "Remember Me", your login will persist for two weeks. If you log out of your account, the login cookies will be removed.

If you edit or publish an article, an additional cookie will be saved in your browser. This cookie includes no personal data and simply indicates the post ID of the article you just edited. It expires after 1 day.

Embedded content from other websites

Articles on this site may include embedded content (e.g. videos, images, articles, etc.). Embedded content from other websites behaves in the exact same way as if the visitor has visited the other website.

These websites may collect data about you, use cookies, embed additional third-party tracking, and monitor your interaction with that embedded content, including tracing your interaction with the embedded content if you have an account and are logged in to that website.

Analytics

We use Google Analytics regularly for monitoring user behavior and traffic sources and utilize the gathered information for enhancing user experience and for business purposes.

The use of Google Analytics in done according to GDPR terms and guidelines provided by Google.

Legal Entity: Techtime.

Primary Contact (a.k.a. "Notification Email Address"): roni@techtime.co.il - this email is designated for receiving notices under the Google Ads Data Processing Terms.

Who we share your data with

We use various cloud platforms and third party providers for the purpose of operating this website.

We do not share or sell your data for any commercial purpose other than specified above.

We use the following processors for the operating this website and executing related digital marketing campaigns:

WP Engine - Hosting Provider

Cloudflare - Cloud based security and web performance processor.

Google Cloud Platform - data centers provider for WP Engine

Sucuri - Website security provider

Mailchimp - Newsletter service provider

Google Analytics, Adwords, Webmasters

Facebook - We use Facebook for advertising and place tracking code on our website for enhancing digital marketing campaigns (i.e - Facebook Pixel).

Planwize Ltd - Digital Marketing Agency.

How long we retain your data

If you leave a comment, the comment and its metadata are retained indefinitely. This is so we can recognize and approve any follow-up comments automatically instead of holding them in a moderation queue.

For users that register on our website (if any), we also store the personal information they provide in their user profile. All users can see, edit, or delete their personal information at any time (except they cannot change their username). Website administrators can also see and edit that information.

What rights you have over your data

If you have an account on this site, or have left comments, you can request to receive an exported file of the personal data we hold about you, including any data you have provided to us. You can also request that we anonymize or erase any personal data we hold about you. This does not include any data we are obliged to keep for administrative, legal, or security purposes.

Request for Receiving Data Associated with One’s Email Address

Users may request to receive access to all related information submitted to this website for their review.

In accordance with GDPR compliance, user may further request the anonymization of such data.

In order to request access for all data associated with a given email address, users may submit the request here. Users then receive an email with a link to a page with all related information.

The link is valid for 24 hours. Users may submit additional request for the same email address once in every 24 hours.

A request for anonymization should be sent separately: User may select the data he or she wishes the site owner to anonymize so it cannot be linked to his or her email address any longer. An email confirmation will be sent once linked data has been successfully anonymized.

Where we send your data

Visitor comments may be checked through an automated spam detection service. All our processors and third party providers comply with GDPR requirements and apply privacy by design and necessary measure to ensure that personal data is being processed and handled in accordance with requirements. The list of our third party service providers and processors is listed above.

Contact information

For all privacy-specific concerns inquiries, you may contact us at mail@mail.com

How we protect your data

We use rigorous practices in order to protect our website and data collected, as well as world class cloud and hosting providers.

Communication between visitor and the server is encrypted using SSL.

The site is protected with web application firewall and is undergoing daily security scans, regular software updates by a dedicated team in order to minimize the risk of data breach.

What data breach procedures we have in place

Once a data breach is detected, our providers execute a dedicated standard operational procedure in order to assess the scope and potential damage, provide immediate remedy, patch any potential security holes and notify users who may be affected by the breach.

We may contact affected users with one or more form of communication within 72 hours and provide the needed information as to the scope of the data breach and actions taken.

What third parties we receive data from

We do not receive data from third parties for our marketing campaigns.

What automated decision making and/or profiling we do with user data

We may apply remarketing/retargeting methods while conducting online advertising using Google Facebook and the likes.

The above is conducted by applying various tracking codes into our website in order to track and retarget users based on

By visiting and using this website you are hereby provide your consent for the use of the above means and methods.